What happened on energy and climate in China this year?

Emissions flatlined; clean power pushed out coal; and oil for transport falls again.

If you want to understand what’s happening on global energy and climate, you need to be following China closely. It’s the world’s largest emitter. It has driven huge amounts of the growth in fossil fuels over the last few decades. At the same time, it’s deploying clean energy technologies at home far faster than any other country, while dominating the supply chains of vital minerals, solar panels, batteries and electric vehicles.1

So here’s a brief round-up of what’s happened in the energy and climate space in China this year.

This will mostly be a summary of the results from the recent publication “China’s Climate Transition: Outlook 2025” by the Centre for Research on Energy and Clean Air (CREA). CREA is an independent research organisation that does incredible work tracking the latest developments in energy across many countries, but they do particularly strong work on making sense of what’s happening in China. We recently had one of its co-founders — Lauri Myllyvirta — on the podcast to discuss China’s position on the energy transition. I also recommend following him on social media to stay up-to-date with the latest.

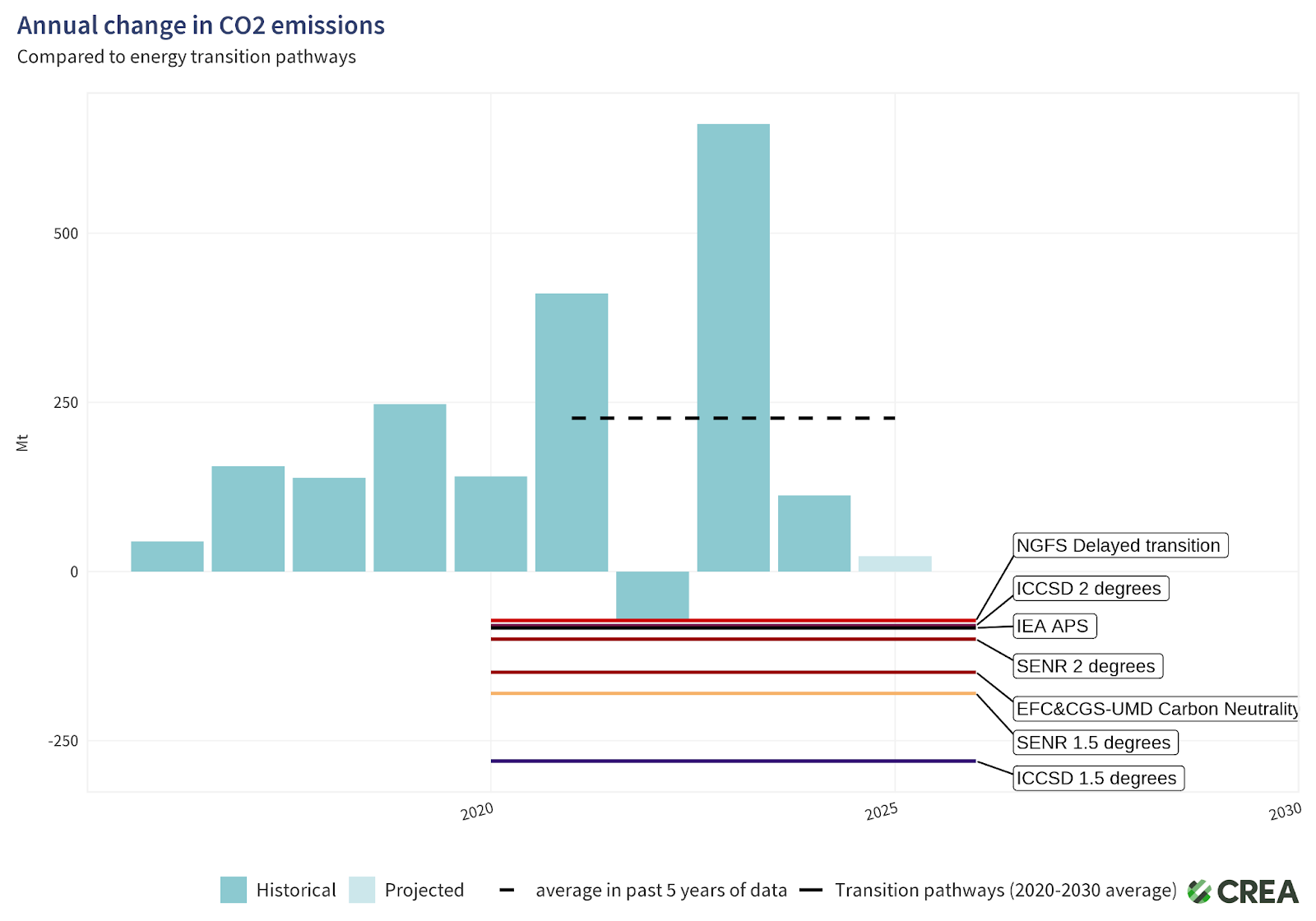

1) China’s total CO2 emissions are expected to stay flat this year

China’s CO2 emissions from all sources — electricity, transport, heating, industry — are basically a plateau with last year’s.

CREA estimates a 0.2% rise, but essentially calls this a plateau, since that rise is incredibly small relative to most years (and the uncertainty in emissions estimates is probably more than 0.2%). You can see this in the chart below, which shows the annual change in CO2 emissions. The last (short) box in the lighter blue is the very small increase in emissions for this year.

China’s emissions have fallen before, but usually during economic downturns or exceptional events like COVID-19. This would really be the first year with little growth in emissions despite strong growth in energy demand. That is, of course, because clean energy sources are also growing quickly and can soak up that extra demand.

This conclusion is similar to the results from the Global Carbon Project. They estimated a slightly larger increase of 0.4% for this year. But they did note that “Given the uncertainty range, a decrease in emissions is also a possibility — confirmation will require full-year data, expected in 2026.”

I’d say “roughly flat emissions” is a fair assessment.

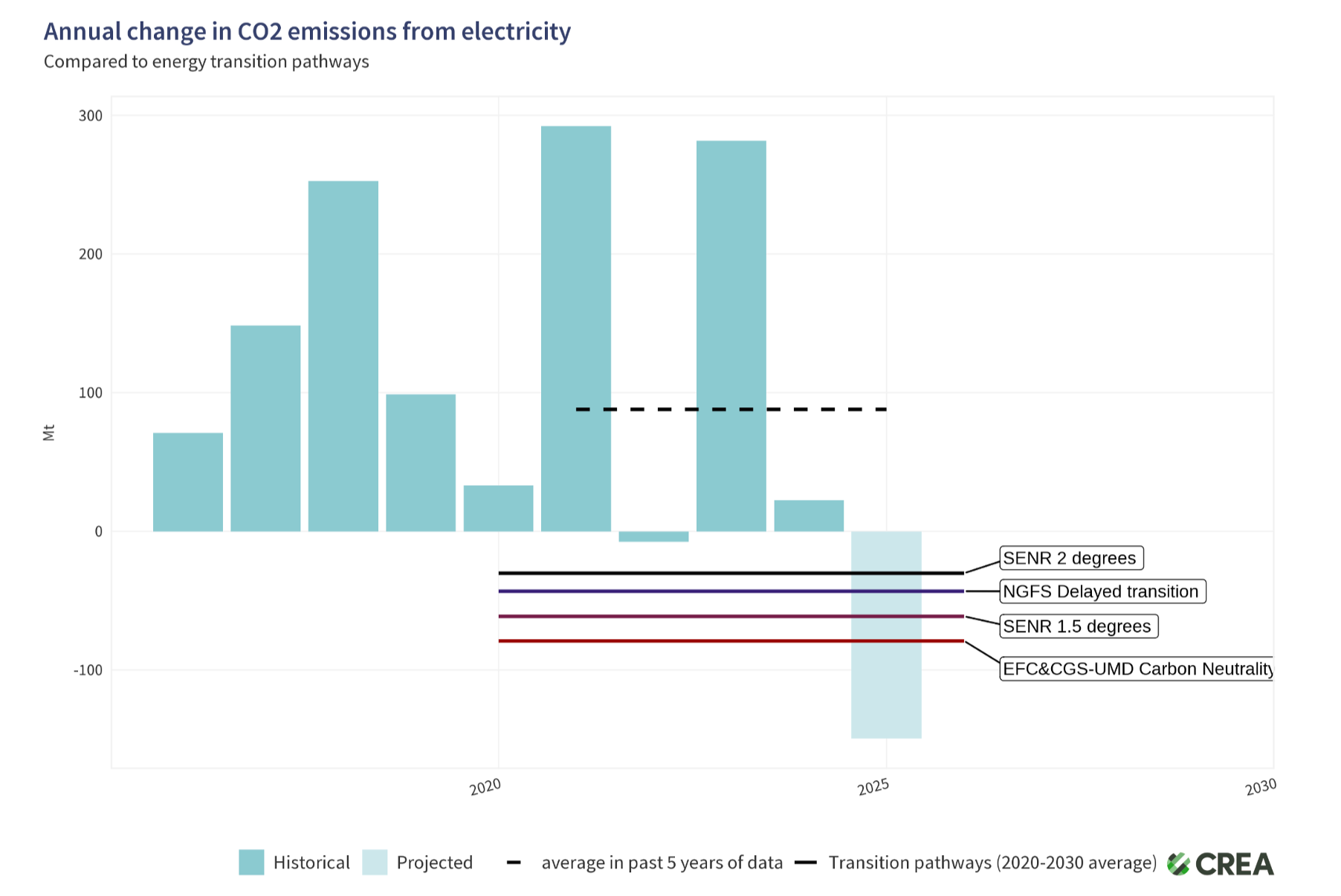

2) CO2 emissions from electricity fell due to the rapid buildout of clean power

Emissions from electricity actually fell this year, despite electricity demand increasing by more than 6%. Data for the first three-quarters of the year indicate a 2% decline.2 You can see this drop for 2025 in the chart below.

In 2024, the increase in emissions from electricity was fairly small. A significant amount of clean power came online, but not quite enough to meet the additional demand. This year, it has been enough.

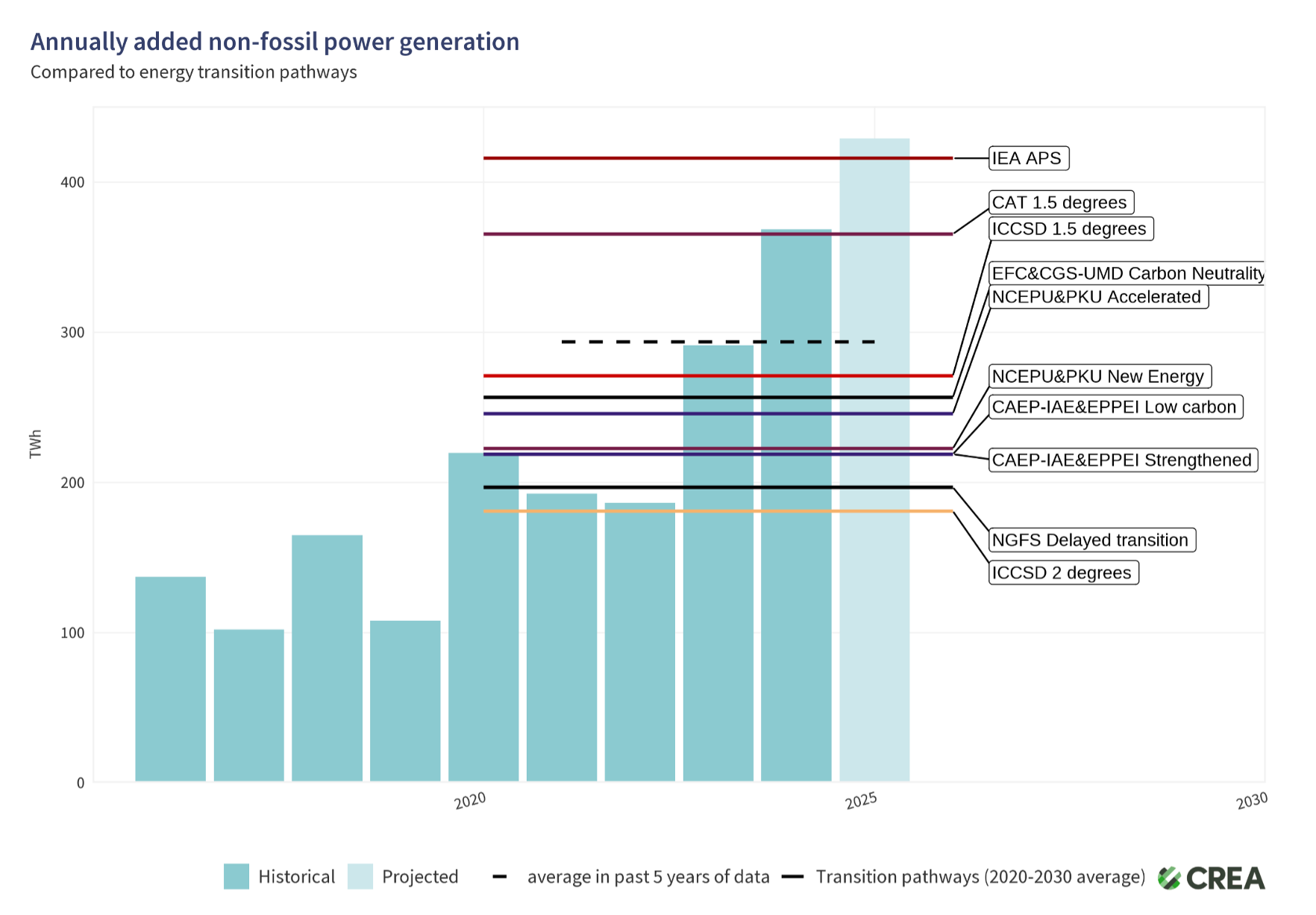

This year, China added around 430 terawatt-hours (TWh) of non-fossil (basically renewables and nuclear) electricity.

This is a lot of new clean power. For context, that’s not far off the total electricity generation of a country like Germany (at around 470 TWh). It’s far more that the total generation of my own country, the United Kingdom (280 TWh), or others like Spain or Australia (which also generate around 280 TWh), or South Africa (245 TWh).

This both highlights how quickly electricity demand in China is increasing. Far more than a UK-sized country every year. And how quickly it’s managing to build clean power.

These results are very much reflected in Ember’s recent reports, which also showed new solar and wind power outpacing electricity demand for the first half of the year. That pushed coal out in absolute terms.

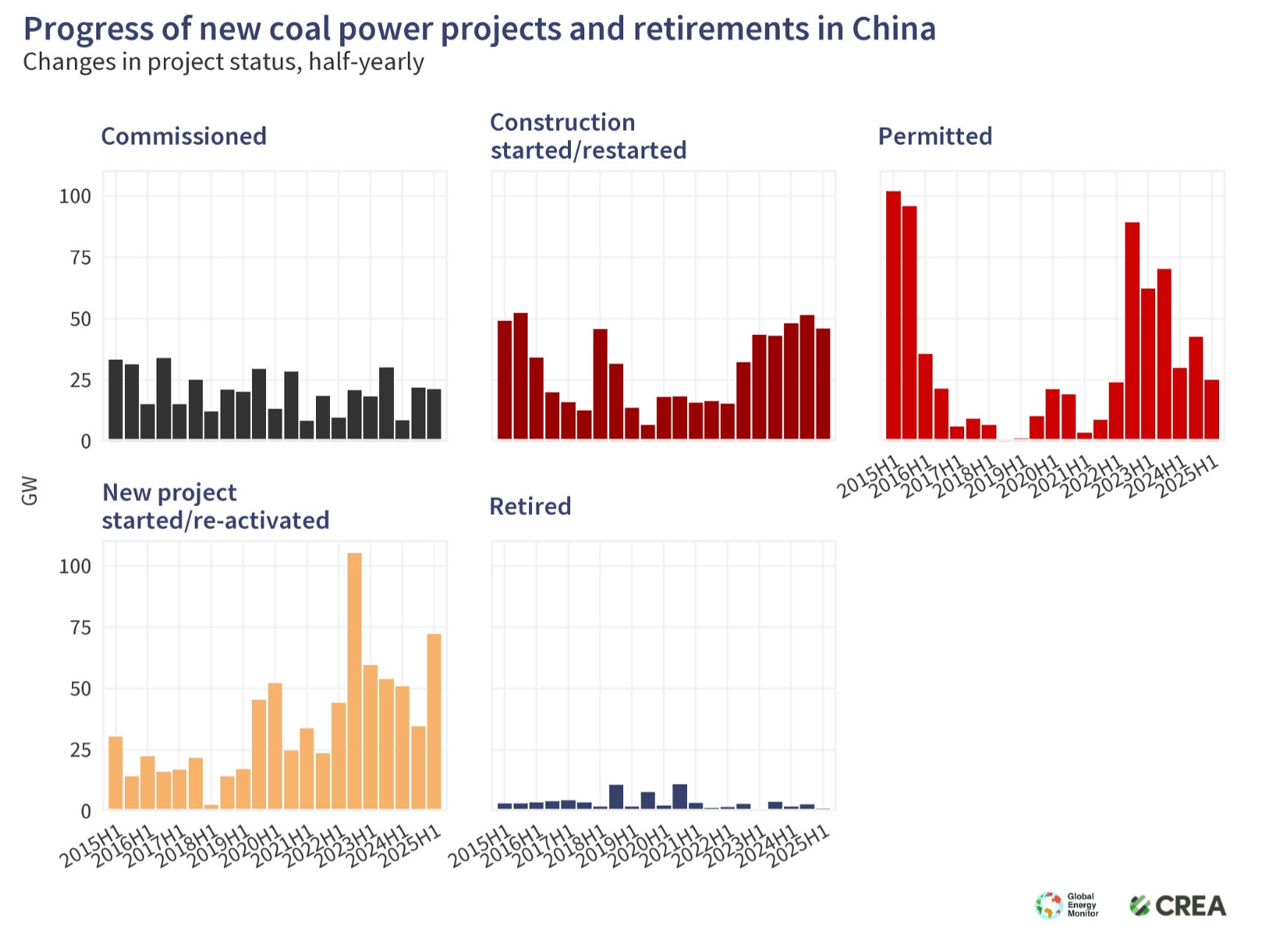

3) China is still building new coal plants

Back to the age-old paradox of why China is building new coal plants, while it’s expanding clean energy so quickly.

It’s true that China is adding new coal capacity. This year, it began construction on new plants, as well as commissioned and approved plans for even more in future years. It also retired very few. This can be quite confusing, as total coal consumption appears to be either at or nearing its peak.

There are several reasons why this paradox exists. First, while China has more and more coal plants, they are running less often. It is possible to have more plants online, while burning less coal at the same time.

Second, some (although not all) of these new coal plants are “peakers”, which are more flexible in ramping power output up or down. This becomes more important in a grid system with variable renewables. In countries like the UK or the US, we tend to do this with gas plants. China is essentially doing the same with coal.

Third, there are several provincial-level incentives for officials to develop new coal capacity. In an earlier post, I described this in more detail, but, as a summary, provinces often act as isolated islands rather than interlinked regions that can work together to ensure supplies. This is inefficient and will probably lead to a lot of redundant capacity and stranded assets.

While from an emissions point-of-view, coal burning, not capacity is the metric that matters, a continued push for new coal plants is still a risk. If they are there, there is inevitably the temptation to use them.

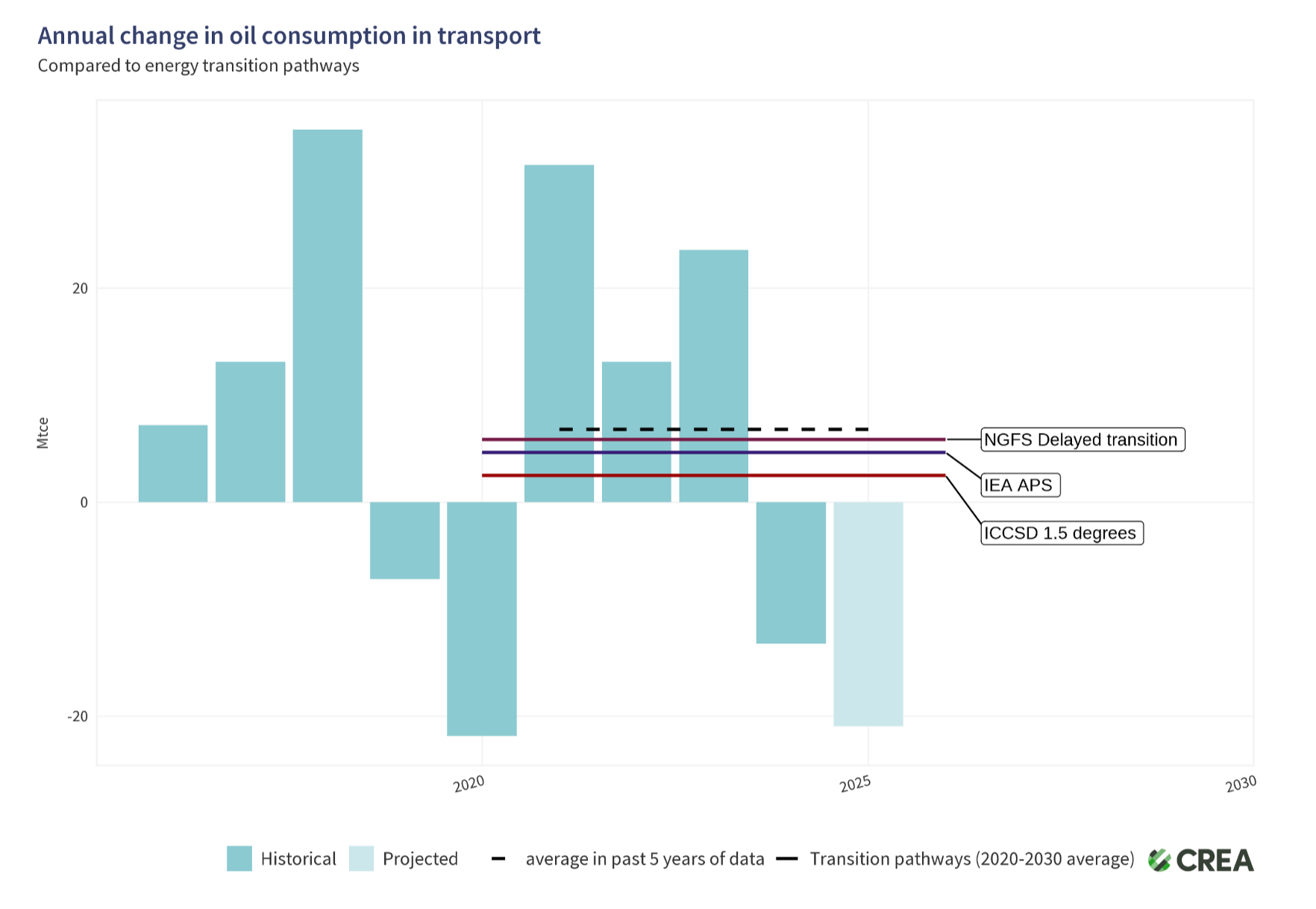

4) Emissions from transport are down thanks to the rapid adoption of electric vehicles

One of the motivations for China to invest in developing a battery and electric vehicle industry was to reduce its dependence on oil. It does not want to stay one of the world’s largest oil importers (and to have to deal with the volatility and insecurity this brings).

It looks like it’s succeeding. Oil consumption for road transport fell last year, and is expected to fall again this year, by 5%. You can see this in the chart below.

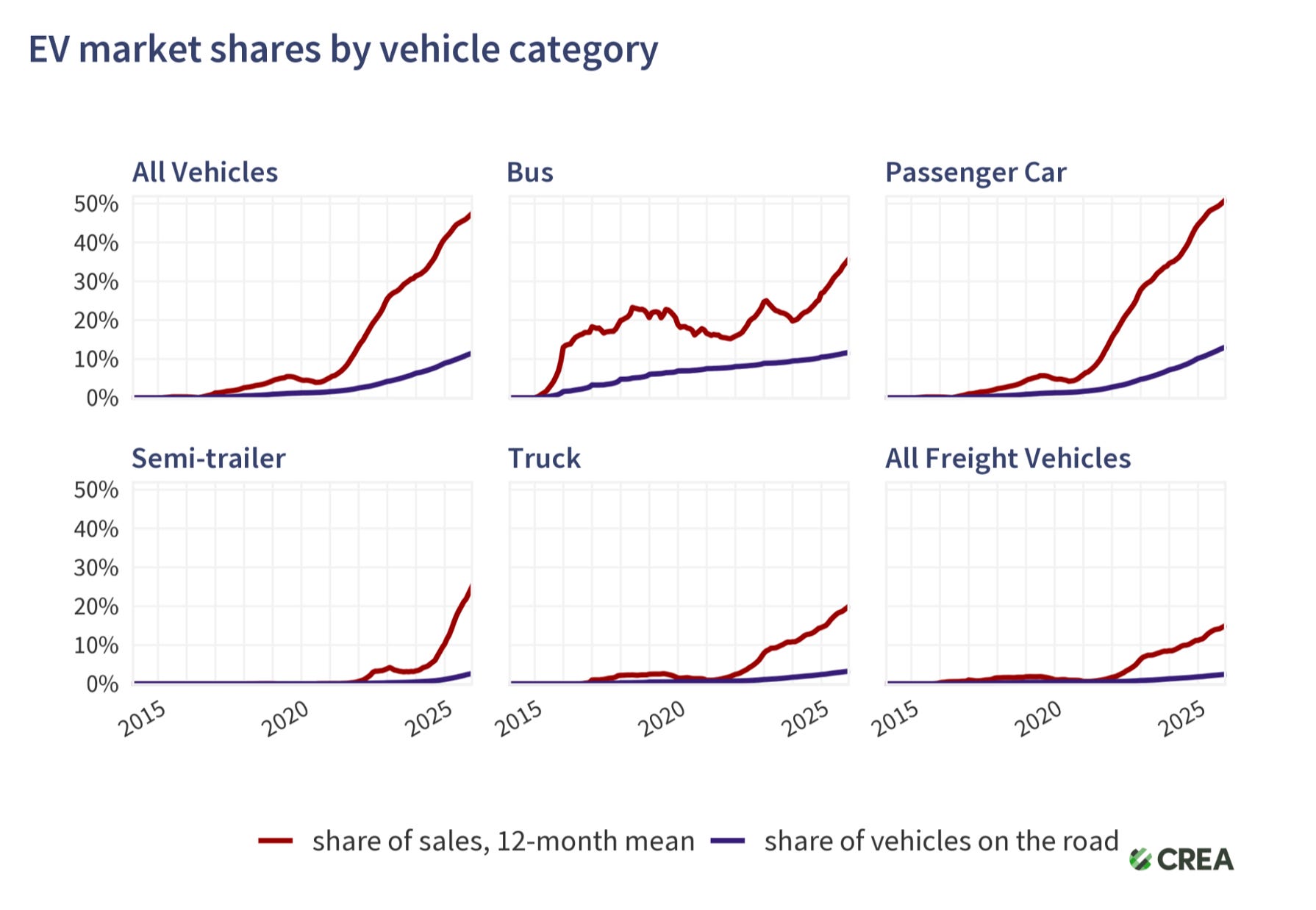

Improvements in energy efficiency play some role in this, but the big structural driver is the rollout of electric vehicles. Below you can see what share of new vehicles (in red), and what share on the road were (in blue) were electric. Note that this includes fully battery-electric vehicles, plug-in hybrids and fuel-cell vehicles (although there are very few of the latter).

More than half of new cars sold in China are electric. 10% on the road are. What’s impressive is how much electrification is happening in other vehicle segments, too. One-in-five new trucks sold are now electric.

Some of the most surprising statistics in the report were about its charging infrastructure. By September this year, there were 18 million charging points installed across the country. That’s up 55% from last year. While some might expect the rollout of chargers to be a purely government-led effort, it is mostly built by private companies. Just 8 companies have over 70% of the market.

China is building an electrified transport system at an incredible speed, and it’s starting to really bite into its oil dependence.

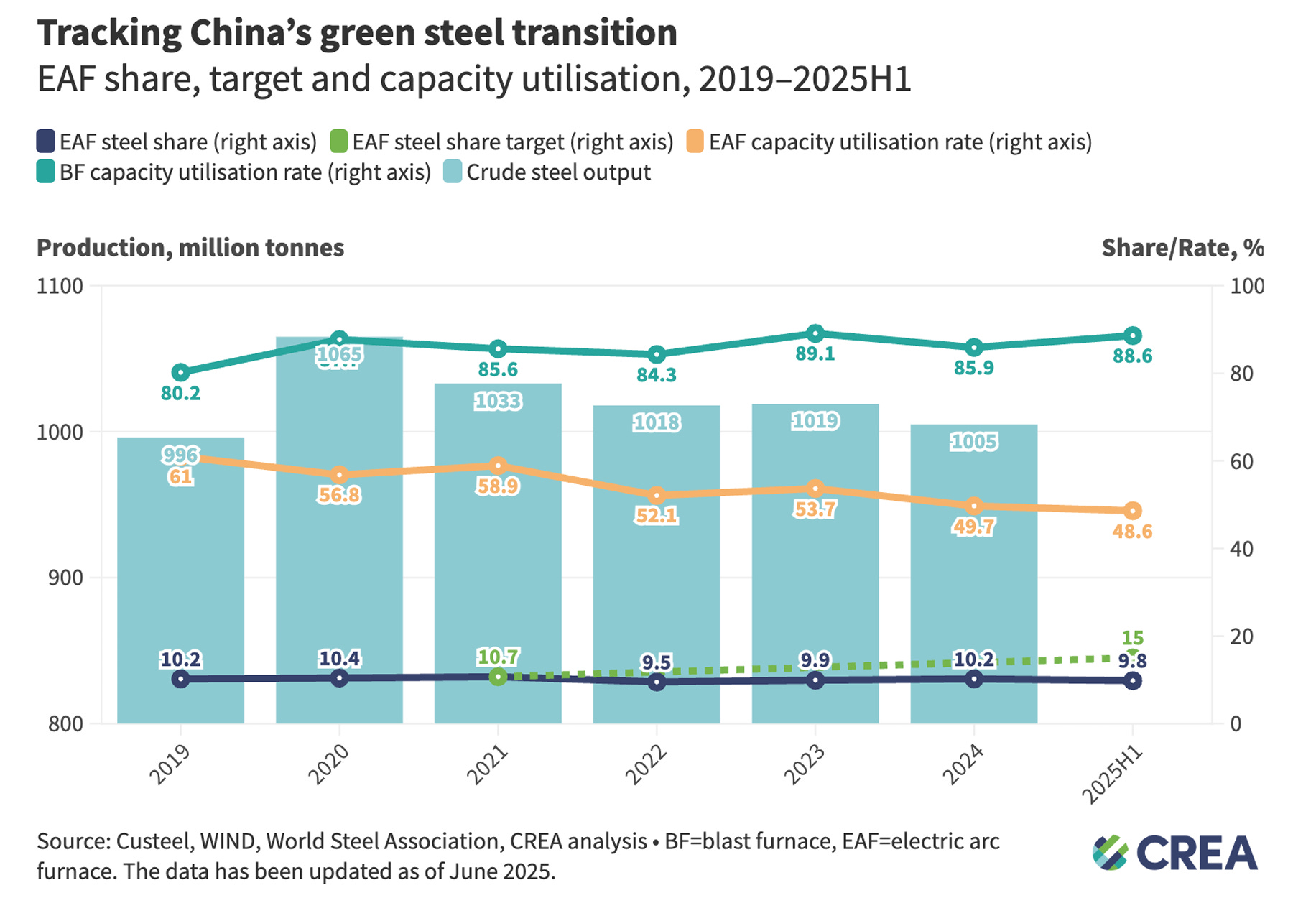

5) Emissions from industry have increased, offsetting the declines in electricity and transport

If carbon emissions from electricity and transport have decreased, why have total emissions stayed flat? Emissions from industry largely offset these reductions. The production of chemicals — which includes products such as plastics and fertilisers — has grown a lot in recent years, and many of these processes rely on coal as a key feedstock.

The adoption of electric arc furnaces — which can eliminate coke consumption in steel production — has been relatively slow. The following chart is quite complex (with lots of acronyms). But the dark blue line shows the share of steel production that comes from electric arc furnaces, which are lower-carbon. It’s still just 10%. Around 90% — shown by the top turquoise line — are blast furnaces, which rely on coke.

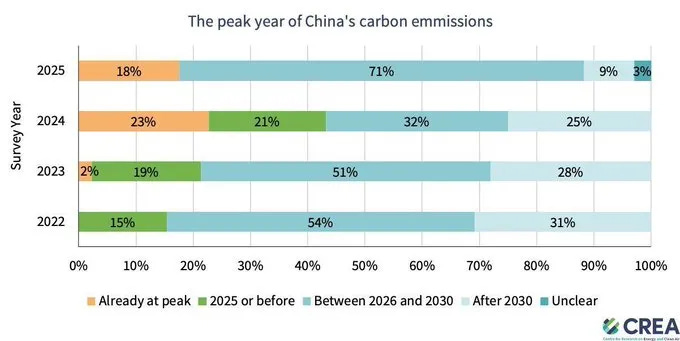

6) It’s always hard to predict a peak

At this point, I think many readers want me to tell them when China’s emissions are going to peak. I’m asked this a lot in interviews (and to be fair, I do my share of asking country-level experts the same).

Looking at the data, there are reasons to be optimistic. Oil consumption for transport appears to be there already. Electricity might be too, although this depends on whether China continues its breakneck speed of solar and wind deployment, and how its growing number of coal plants are utilised.

Policies and innovation in industrial processes lag behind (like they do across most of the world), and we might expect emissions from these sectors to continue to increase for some years.

How all of this falls out is hard to predict. Some analysts believe the peak has already arrived. Others, a few years yet. Most, though, seem fairly confident that it will be before the end of the decade.

The key thing about a peak is that it’s not obvious until several years after the fact. Emissions falling for one, or even two, years is not enough to be confident that they don’t rebound. What gives more confidence alongside the emissions data is the underlying structural drivers of these changes. With the rapid growth in electric cars, for example, it’s hard to see the combustion engine making a comeback.

→ Read CREA’s report in full.

→ Listen to our podcast episode with CREA co-founder, Lauri Myllyvirta

This is based on total clean energy deployment. As I showed in a previous article, when looking at this on a per capita basis, its rates are less exceptional.

Of course, 2025 is not over so getting annual figures depends on some expectations of how the final few months have gone, or will go. Changes over this period are unlikely to change the direction of change (from a decline to an increase).